Money moves differently now. Not slowly. Not through paperwork. Just quick taps on a phone.

Someone pays the dinner bill. Another person sends rent. A friend transfers money for a birthday gift. Seconds later, done. No bank visit. No waiting.

That’s the quiet power of P2P payment apps. And people are using them everywhere.

The global P2P payment market is expected to reach $21.42 billion by 2030, growing at a CAGR of 7.2%. That number alone tells you something important. Users don’t just like digital payments anymore; they expect them.

Instant transfers. Clean interfaces. No friction. For fintech startups, banks, and even non-financial businesses, this shift opens a big opportunity. But it also raises a practical question.

What does it actually take to build a P2P payment app people trust?

Because building one is not just about coding a transfer button. It’s about security. Compliance. Infrastructure. User psychology. And a lot of careful decisions in between.

So before jumping into development, first understand its basics:

How these apps work. Why users rely on them. And what features they now consider non-negotiable.

What Is a P2P Payment App?

At its simplest, a P2P payment app lets people send money directly to other people. No middlemen handling paperwork. No long processing times. Just a direct transfer from one account to another.

Usually, the process is simple:

- Enter a phone number.

- Choose a contact.

- Scan a QR code.

- Confirm the amount.

Done.

Behind that simplicity, though, a lot is happening. Bank integrations. Payment networks. Security checks. Identity verification. All working quietly in the background. What makes P2P payment transfer apps so powerful is how they remove the friction that used to exist in financial transactions.

As a result, Geography becomes less important. Banking hours stop mattering. And even small payments become effortless.

How Do P2P Payment Apps Work?

From the outside, a P2P payment app feels almost too easy.

Tap > Enter amount > Send > Money transferred and done.

But under the surface? A lot is happening. Quietly. Very fast. Good P2P payment app development hides the complexity. Users only see the smooth part. The frictionless part. The part that feels like sending a text message.

But when companies plan to build a P2P payment app, they must understand the full transaction flow. Every step matters. Security. Infrastructure. Banking rails. Compliance.

Let’s slow it down a little.

- Account Linking

Every P2P payment transfer app starts here. Users connect a funding source. Usually: bank account, debit card, credit card, or a digital wallet.

During this step, the platform also verifies the user. Sometimes quickly. Sometimes with extra checks. Depends on regulations.

You’ll usually see things like:

- OTP verification.

- Phone number validation.

- Email confirmation.

- Sometimes, biometric checks.

And then there’s KYC verification. This part is important. Financial platforms must confirm the user’s identity before allowing transactions.

Yes, it adds friction. But skipping it? Not an option.

- Authentication

Now comes the security layer. A serious P2P payment app cannot rely on just passwords. Too risky. Too outdated. So most apps add extra authentication layers like: Fingerprint login. Face recognition. Device-based verification. Or OTP security.

Some platforms even track device behavior. Sounds complicated. But users barely notice. They just feel protected. And honestly, when money is involved, that reassurance matters.

- Payment Initiation

This is the part users actually interact with. The sender chooses the recipient. Simple options usually work best: Phone number. Username. Saved contacts. QR code scanning.

Good P2P payment app development makes this step feel natural. Almost casual. Like sending a chat message. No confusion. No complicated forms.

Just select → enter amount → confirm. Done.

The smoother this step feels, the more people use the app. That’s why UX design plays a huge role when businesses build a P2P payment app. Finance should not feel intimidating.

- Transaction Processing

Now the invisible systems take over. As soon as the user confirms the payment, the app encrypts the transaction data. Immediately. Then the request travels through: Payment gateways. Banking APIs. Card networks. Real-time payment infrastructure.

Depending on the region, the transfer may settle instantly. Or within minutes. Some countries support real-time clearing networks. Others rely on near-real-time settlement. This is one of the most technically demanding parts of P2P payment app development.

Integrations must be reliable. Scalable. Secure. Because if transactions fail, users panic. And they instantly uninstall the app.

- Fraud Detection

While the payment travels through the network, something else is happening quietly. Fraud monitoring. Modern P2P payment platforms constantly scan transactions in real time. They watch for unusual patterns.

For example: Sudden high-value transfers. Multiple payments in seconds. Login attempts from strange locations. New devices are sending money immediately.

If something feels suspicious, the system may pause the payment. Or request extra verification. Most users never notice these systems. Which means they’re working perfectly.

- Confirmation and Transaction Records

Once the payment clears, the system sends confirmation to both users. Usually through: Push notifications. In-app transaction updates. Payment receipts. These confirmations matter more than people realize.

When money moves, people want certainty. Not assumptions. Not guesswork. So a good P2P payment transfer app always shows:

- Transaction history.

- Time stamps.

- Payment IDs.

- Sender and receiver details.

In short, transparency builds trust. And trust is the real currency of digital payments. What actually powers a P2P payment app? Users see a simple interface. That’s intentional. All synchronized. And all working in milliseconds.

This is why companies planning to build a P2P payment app often partner with experienced fintech development teams. The architecture is deeper than it looks.

Key Features Users Expect in P2P Payment App

User expectations in the finance industry are unusually high, and understandably so. When people trust an app with their money, tolerance for friction drops dramatically.

- Instant Transfers

Speed is foundational. Whether the transfer happens in seconds or minutes, users expect minimal delay and clear confirmation once funds move.

- Strong Security Measures

Biometric login, end-to-end encryption, and fraud monitoring are no longer premium features. They are baseline requirements.

- Simple Onboarding

Lengthy registration flows often lead to drop-offs. The strongest apps streamline verification without weakening compliance.

- Contact-Based Payments

Sending money should feel natural. Phone numbers, usernames, or QR codes eliminate the need for memorizing account details.

- Transparent Transaction History

Users want visibility. Clear records build confidence and simplify personal finance tracking.

- Notifications in Real Time

Immediate alerts reassure both sender and receiver that the transaction has been completed.

- Split Payments

From shared travel expenses to group dinners, built-in splitting features reduce awkward calculations and follow-ups.

- Multi-Bank Support

Flexibility strengthens adoption. Users prefer platforms that integrate smoothly with multiple financial institutions.

Individually, these features improve usability. Together, they create trust, the currency every fintech platform depends on.

Types of P2P Payment Apps

Not all P2P platforms operate the same way. Their structure often reflects the audience they intend to serve.

- Bank-Centric Apps

These apps are usually developed by traditional banks or large financial institutions. Stability comes first. Compliance too. Everything is tightly aligned with financial regulations. Users tend to trust these P2P payment apps quickly.

Why?

Because the bank already holds credibility. People are already familiar with the brand. That trust shortens the adoption curve. Most bank-centric platforms focus on secure domestic transfers, account-to-account payments, and seamless bank integrations.

- Standalone Wallet-Based Apps

This is where many fintech startups operate. These digital wallet P2P payment apps allow users to store funds directly inside the platform before transferring money.

The experience feels flexible. Fast. Sometimes even fun. Beyond basic transfers, these platforms often add features like rewards programs, merchant payments, cashback offers, or small micro-transactions.

- Social Payment Apps

This category mixes finance with communication. Which sounds unusual at first, but users actually love it.

A social P2P payment app allows people to send money while interacting with friends. Users may attach notes, emojis, comments, or even public payment feeds. Transactions start to feel conversational.

- Cross-Border Payment Platforms

Then there are platforms built for international money movement. A completely different challenge.

These cross-border P2P payment apps focus heavily on currency exchange, compliance across countries, and transaction cost efficiency. Sending money globally requires more infrastructure. More regulation. More security layers.

How to Build a P2P Payment App

Building a P2P payment app is not just a coding project. A lot of people assume that, actually. Write some code. Connect a payment gateway. Launch the app. Done.

Not really.

Real P2P payment app development includes strategic thinking. Sometimes time-taking. It touches compliance, banking infrastructure, UX psychology, and security architecture, all at once.

Let’s walk through it:

- Discovery and Market Validation

Every successful P2P payment app development project begins with clarity.

Simple questions first.

- Who are the users? Students? Freelancers? Businesses?

- Local payments or global transfers?

Then the harder question: Why would someone use this app instead of the ten others already available?

This stage often involves: Market research. Competitor analysis. User behavior studies. Business model definition. Because yes, P2P payment transfer apps exist everywhere now. But usage patterns change depending on geography.

Understanding these patterns early helps companies build a P2P payment app that actually fits the market. Skipping this stage usually leads to expensive pivots later.

- Regulatory and Compliance Planning

This is the part many startups underestimate. Finance is not like other apps. You cannot just launch and “figure it out later”. Every P2P payment app development project must address regulations from the beginning.

That includes things like:

- KYC (Know Your Customer) verification

- AML (Anti-Money Laundering) protocols

- Data protection laws

- Financial licensing requirements

Depending on the region, these rules can change significantly. Some countries require strict identity checks. Others impose transaction limits. Some require partnerships with licensed banks.

Compliance isn’t a small step at the end. It’s architectural. If ignored, the entire P2P payment app launch can get delayed. Or worse, blocked. And credibility? That’s very hard to recover once damaged.

- UI/UX Architecture

Now comes the user experience. When money moves, people become cautious. Even small confusion can create chaos.

That’s why good P2P payment app development services focus heavily on UI/UX design. User journeys must feel obvious. Not complicated. Not cluttered. Just clear.

The best P2P payment apps focus on reducing steps. A payment flow might look like this:

Select contact > Enter amount > Confirm payment.

That’s it. But behind that simplicity sits careful design thinking. Confirmation screens. Transaction receipts. Error handling. Clear feedback. Good fintech UX is rarely flashy.

- Core Development and Integrations

Once the strategy and UX are ready, the real P2P payment app development work begins. Developers start building the core infrastructure. This usually involves integrating several financial systems, such as:

- Payment gateways

- Banking APIs

- Identity verification services

- Fraud monitoring tools

- Encryption protocols

These integrations power the P2P payment transfer app behind the scenes. At the same time, engineers build the backend architecture that handles transactions, user data, and payment requests. Scalability becomes critical here.

An app that works for 10,000 users should still perform smoothly at 100,000 users. Or even a million. Because when payment platforms grow quickly, and they often do, weak infrastructure becomes painfully visible.

- Testing and Security Reinforcement

Before launch, the app is pushed to its limits.

Teams simulate transaction spikes, unstable networks, device variations, and potential fraud scenarios. Security audits run alongside performance testing to ensure resilience. Because in fintech, trust is fragile and difficult to rebuild once lost.

- Launch and Continuous Improvement

Launching the app feels exciting. But it’s not the end. Honestly, it’s the beginning. Once users start interacting with the P2P payment app, real insights appear. Analytics reveal friction points. Drop-offs show where users get confused. Support requests highlight missing features.

This feedback loop helps teams improve the platform continuously. New security threats emerge. Payment behaviors evolve. Financial regulations change. The best companies treat P2P payment app development as an ongoing process, not a one-time project.

They iterate. Improve. Adapt. Because the digital payments landscape moves fast. And the apps that survive long-term are the ones that keep evolving.

Security & Compliance Requirements in P2P App Development

In most apps, security is important. In fintech, it is foundational.

Users are not just sharing data; they are trusting the platform with their money. One vulnerability can undo years of credibility. That is why security must be embedded into the architecture from the very beginning, not layered on after development.

- Regulatory Compliance

Financial ecosystems operate under strict regulatory frameworks that vary by region. Depending on your target market, requirements may include:

- KYC (Know Your Customer): Verifies user identities to prevent fraud.

- AML (Anti-Money Laundering): Detects suspicious transaction patterns.

- GDPR or data protection laws: Ensure responsible handling of personal information.

- PCI DSS compliance: Mandatory for platforms processing card payments.

Compliance may feel like friction during development, but it protects the business from far greater disruption later.

- Encryption and Data Protection

Sensitive information should never travel unprotected.

End-to-end encryption, tokenization, and secure key management help ensure that even if data is intercepted, it remains unreadable.

Many platforms also adopt zero-trust architectures, where every access request is verified, regardless of origin.

- Multi-Factor Authentication

Passwords alone no longer provide adequate protection.

Combining authentication layers, OTPs, biometrics, or device-based verification dramatically reduces unauthorized access risks.

From a user perspective, these steps signal seriousness. Security features often double as trust signals.

- Fraud Detection Systems

Modern P2P payment apps rely heavily on intelligent monitoring tools that flag unusual behavior in real time.

For example:

- Rapid transaction spikes

- Logins from unfamiliar locations

- Suspicious payment patterns

Early detection allows platforms to intervene before damage occurs.

- Continuous Security Audits

Threat landscapes evolve constantly. What is secure today may become vulnerable tomorrow.

Regular penetration testing, code reviews, and infrastructure audits help platforms stay ahead of emerging risks.

Because in digital finance, prevention is always cheaper than recovery.

How Much Does It Cost to Build a P2P Payment App

This is often the first question stakeholders ask, sometimes before the idea is fully formed.

“How much will it cost?”

The honest answer: it depends on what you are building, who you are building it for, and how ambitious the platform is meant to become.

Scope defines effort. Effort defines investment.

Let’s look at realistic ranges.

- MVP Development ($30K – $60K)

This is the starting line for many startups.

An MVP development focuses strictly on core capabilities:

- User registration and verification

- Bank or card linking

- Secure money transfers

- Transaction history

- Basic notifications

- Admin controls

Design remains clean but practical. Integrations stay limited to reduce complexity. The goal here is not perfection; it is validation. Real users. Real transactions. Real feedback. Launching lean allows businesses to learn before scaling.

- Mid-Level App ($60K – $120K)

Now the platform begins to mature.

Expect stronger UI/UX refinement, faster navigation, expanded payment options, and improved dashboards. Security layers grow deeper. Infrastructure becomes more resilient.

Additional capabilities may include:

- Split payments

- Advanced fraud detection

- Multi-bank integrations

- Enhanced analytics

- Customer support modules

This range often suits growing fintech companies preparing for broader adoption.

- Advanced Platform ($120K+)

At this level, the product is built to lead rather than follow.

Architecture is deeply scalable. Compliance frameworks are robust. Automation supports operational efficiency.

Advanced platforms may introduce:

- AI-driven fraud monitoring

- Cross-border payments

- Multi-currency support

- Predictive analytics

- Open banking integrations

While the upfront investment is higher, these systems often reduce operational friction over time and position the business for long-term growth.

Hidden Costs Businesses Should Anticipate

Many teams plan for development but underestimate what follows.

Common post-launch expenses include:

- Ongoing maintenance and updates

- Cloud infrastructure scaling

- Security audits

- Regulatory renewals

- Customer support operations

Budgeting for these early prevents unpleasant surprises later.

One important perspective: the cheapest build rarely becomes the most economical in the long run. Stability, security, and scalability deliver far greater returns than short-term savings.

When money moves through your platform, reliability becomes your brand.

And that is always worth investing in.

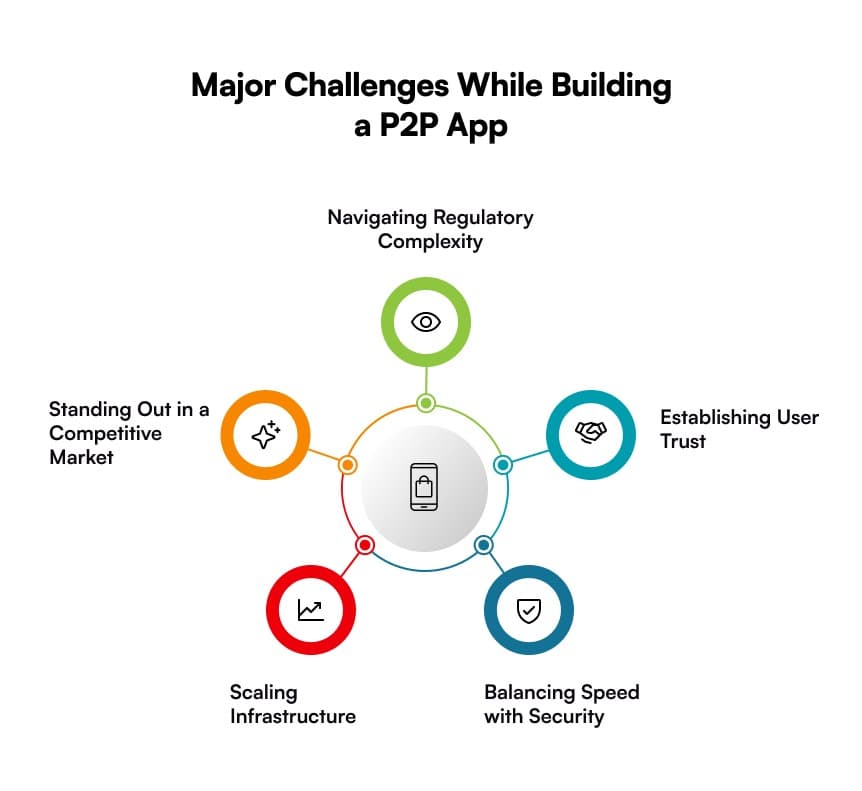

Major Challenges While Building a P2P App

Building a P2P payment app is as much about risk management as it is about innovation. The opportunity is substantial, but so is the responsibility.

Here are some of the most common hurdles businesses encounter.

- Navigating Regulatory Complexity

Financial regulations differ across regions and evolve frequently. Licensing, KYC mandates, AML requirements, and data protection laws demand ongoing attention.

Compliance is not a one-time milestone. It is a continuous operational commitment. Ignoring it can delay launches or worse, invite legal exposure.

- Establishing User Trust

People hesitate before trusting a new platform with their money. And rightly so. A single failed transaction or security scare can push users toward competitors permanently.

Trust is built through consistency:

- Reliable uptime

- Transparent communication

- Visible security measures

- Fast dispute resolution

Fintech loyalty is fragile but incredibly valuable once earned.

- Balancing Speed with Security

Users want instant transfers. Security protocols, however, require careful verification. Striking the right balance is critical. Too many checks create friction. Too few create vulnerability. The strongest platforms make security feel seamless rather than obstructive.

- Scaling Infrastructure

Transaction spikes rarely arrive with warning; festive seasons, promotional campaigns, or viral adoption can strain systems overnight.

Without a scalable architecture, performance suffers. And in payments, even a few seconds of delay can trigger user anxiety. Planning for growth before it arrives is always cheaper than rebuilding afterwards.

- Standing Out in a Competitive Market

The fintech space is crowded. New entrants compete not only with startups but also with established banks and global payment giants. Differentiation often comes down to experience, smoother onboarding, smarter features, and faster support.

Technology alone rarely wins. Execution does.

P2P Payment App Monetization Strategies: How These Platforms Generate Revenue

A P2P payment app may begin as a convenience tool, but sustainable growth depends on a clear revenue model.

Interestingly, many successful platforms monetize quietly, ensuring the user experience never feels transactional.

- Transaction Fees

A small fee on instant transfers, credit-based payments, or cross-border transactions can generate steady revenue without overwhelming users.

The key is transparency. Hidden charges erode trust quickly.

- Merchant Services

Once adoption grows, enabling businesses to accept payments through the platform opens a powerful revenue stream.

Merchant partnerships often lead to:

- Processing fees

- Subscription models

- Value-added services

It transforms the app from a payment tool into a commerce enabler.

- Premium Features

Some users are willing to pay for convenience, faster transfers, advanced analytics, higher limits, or enhanced security controls. A freemium model allows broad adoption while creating optional upgrade paths.

- Interest on Wallet Balances

When users store funds within the platform, those balances can generate interest depending on regulatory allowances. Individually small. Collectively meaningful.

- Financial Ecosystem Expansion

Over time, many P2P apps evolve into broader financial hubs offering lending, insurance, investments, or budgeting tools. The strategy is simple: once trust is established, adjacent services feel natural. Revenue follows engagement.

Future Trends in P2P Payment Apps

The next phase of P2P payments will not just be faster, it will be smarter, more embedded, and increasingly invisible.

- AI-Driven Fraud Prevention

Machine learning models are already improving threat detection by identifying suspicious behavior before transactions finalize. Security is shifting from reactive to predictive.

- Biometric Authentication

Passwords are gradually giving way to fingerprint scans, facial recognition, and behavioral biometrics, reducing friction while strengthening protection. Convenience and security are finally aligning.

- Embedded Finance

Payments are moving beyond standalone apps into marketplaces, ride-sharing platforms, creator ecosystems, and social environments. Soon, users may not even think of it as a “payment.” It will simply be part of the experience.

- Cross-Border Simplicity

Global workforces and digital commerce are increasing the demand for low-cost international transfers. Platforms that simplify currency exchange and compliance will gain a strong competitive edge.

- Open Banking Expansion

As financial institutions expose APIs, fintech platforms gain deeper access to banking capabilities, unlocking innovation that was difficult just a few years ago. Collaboration is quietly replacing competition.

Concluding Words

Building a P2P payment app is not just another software project. It’s bigger than that. A strategic move, actually. Finance, security, infrastructure, and user experience all come here. And yes, scalability too. Because if the platform grows, the system must grow with it. No excuses.

Companies often jump in thinking P2P payment app development is mainly about coding a payment feature. It isn’t. Not even close. It’s about building trust.

For businesses thinking about entering this space, the opportunity is huge. Digital payments keep expanding. Fintech adoption keeps accelerating. But success doesn’t happen by accident. Companies need a clear strategy.

This is where working with an experienced P2P payment app development company becomes critical. Not just developers. Real fintech specialists who understand payment infrastructure, banking APIs, fraud prevention, compliance requirements, and the whole system.

At Galaxy Weblinks, we work with businesses that want to build serious fintech products. Not experiments. Not half-ready apps. We help organizations design and develop secure, scalable P2P payment apps built for real-world usage.

If you’re exploring how to build a P2P payment app or thinking about upgrading an existing digital payment platform, the right development partner can shorten the journey. Less risk. Faster execution. Stronger architecture.

Because launching a fintech product isn’t just about technology. It’s about confidence.

FAQs

1. How long does it take to build a P2P payment app?

Timelines vary based on complexity. A focused MVP may take around 3–6 months, while advanced platforms with deeper integrations can extend beyond that. Structured planning often saves more time than rushing development.

2. Is regulatory compliance mandatory for P2P apps?

Absolutely. Financial platforms must adhere to regional regulations such as KYC, AML, and data protection standards. Compliance protects both the business and its users.

3. Should startups begin with an MVP?

In most cases, yes. An MVP allows businesses to validate demand, gather real user feedback, and refine the product before committing to large-scale investment.

4. What is the most critical feature in a P2P payment app?

Security. Without it, adoption stalls. Users need confidence that their data and money are protected at every step.

5. Can a P2P payment app scale as the user base grows?

Yes, provided scalability is planned early. Cloud infrastructure, modular architecture, and strong backend systems ensure the platform can handle increasing transaction volumes smoothly.

6. How do businesses choose the right development partner?

Look beyond coding ability. Evaluate fintech experience, regulatory understanding, architectural thinking, and post-launch support. A strong partner does more than build; they guide strategic decisions.